EUR/USD: The EUR faces challenges from domestic economic struggles and global geopolitical risks. However, it appears oversold and undervalued. Economists expect no Eurozone recession and project an ECB terminal rate of 2.25%, above market expectations. Political stability post-German elections and potential de-escalation in Ukraine could ease risks, boosting Eurozone demand. EUR/USD may stay grounded in 3-6 months but recover cautiously in 6-12 months.

USD: While the USD weakened post-Trump’s inauguration, it may regain ground as trade war risks escalate. However, positives are largely priced in, and we expect the USD to remain near recent highs into early 2025 but decline long-term due to Fed rate cuts, fiscal concerns, and a potential return of Trump’s “Weak USD Doctrine” by H2 2025.

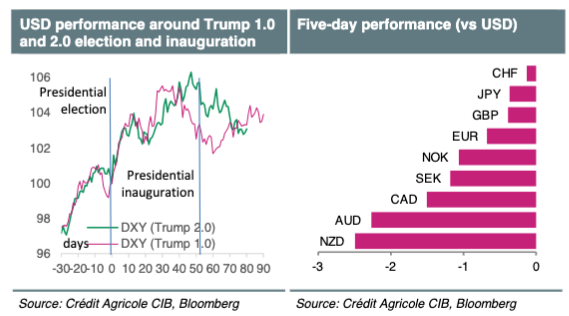

CHF: Safe-haven flows have bolstered the CHF amid Eurozone uncertainties. Once risks subside, the CHF could return as a funding currency, supported by near-zero rates and high valuations. The SNB will monitor FX developments amid Swiss disinflation.

JPY: The JPY remains resilient, with the US-Japan rate spread narrowing as the Fed cuts rates and the BoJ hikes. This reduces USD/JPY carry appeal, with volatility likely to persist due to rate path uncertainties and Trump’s trade policies. Japan’s MoF may intervene to support the JPY.

GBP: UK economic concerns and high borrowing costs could necessitate austerity, creating headwinds. However, political stability and economic outperformance relative to the Eurozone support GBP as a higher-yielding EUR proxy. GBP/EUR is constructive for 2025-2026, while GBP/USD may recover in 2026 after initial struggles.

CAD: USD/CAD hit highs above 1.45 due to Trump’s tariffs, but risks remain tilted downward for CAD in early 2025 amid a wider BoC-Fed rate gap. Canada’s relative growth outperformance could aid a gradual CAD recovery.

AUD/USD: Trump’s China tariffs and a falling rate differential weakened AUD/USD, but softer tariffs and less dovish RBA policy could provide support.

NZD/USD: NZD/USD was pressured by China tariffs, a falling NZ-US rate differential, and dry weather. Lower-than-expected tariffs, stable rate differentials, La Niña, and NZ growth rebound should support NZD/USD.

EUR/USD: The EUR faces challenges from domestic economic struggles and global geopolitical risks. However, it appears oversold and undervalued. Economists expect no Eurozone recession and project an ECB terminal rate of 2.25%, above market expectations. Political stability post-German elections and potential de-escalation in Ukraine could ease risks, boosting Eurozone demand. EUR/USD may stay grounded in 3-6 months but recover cautiously in 6-12 months.

USD: While the USD weakened post-Trump’s inauguration, it may regain ground as trade war risks escalate. However, positives are largely priced in, and we expect the USD to remain near recent highs into early 2025 but decline long-term due to Fed rate cuts, fiscal concerns, and a potential return of Trump’s “Weak USD Doctrine” by H2 2025.

CHF: Safe-haven flows have bolstered the CHF amid Eurozone uncertainties. Once risks subside, the CHF could return as a funding currency, supported by near-zero rates and high valuations. The SNB will monitor FX developments amid Swiss disinflation.

JPY: The JPY remains resilient, with the US-Japan rate spread narrowing as the Fed cuts rates and the BoJ hikes. This reduces USD/JPY carry appeal, with volatility likely to persist due to rate path uncertainties and Trump’s trade policies. Japan’s MoF may intervene to support the JPY.

GBP: UK economic concerns and high borrowing costs could necessitate austerity, creating headwinds. However, political stability and economic outperformance relative to the Eurozone support GBP as a higher-yielding EUR proxy. GBP/EUR is constructive for 2025-2026, while GBP/USD may recover in 2026 after initial struggles.

CAD: USD/CAD hit highs above 1.45 due to Trump’s tariffs, but risks remain tilted downward for CAD in early 2025 amid a wider BoC-Fed rate gap. Canada’s relative growth outperformance could aid a gradual CAD recovery.

AUD/USD: Trump’s China tariffs and a falling rate differential weakened AUD/USD, but softer tariffs and less dovish RBA policy could provide support.

NZD/USD: NZD/USD was pressured by China tariffs, a falling NZ-US rate differential, and dry weather. Lower-than-expected tariffs, stable rate differentials, La Niña, and NZ growth rebound should support NZD/USD.Institutional Insights: Credit Agricole FX Weekly 28/02/25

EUR/USD: The EUR faces challenges from domestic economic struggles and global geopolitical risks. However, it appears oversold and undervalued. Economists expect no Eurozone recession and project an ECB terminal rate of 2.25%, above market expectations. Political stability post-German elections and potential de-escalation in Ukraine could ease risks, boosting Eurozone demand. EUR/USD may stay grounded in 3-6 months but recover cautiously in 6-12 months.

USD: While the USD weakened post-Trump’s inauguration, it may regain ground as trade war risks escalate. However, positives are largely priced in, and we expect the USD to remain near recent highs into early 2025 but decline long-term due to Fed rate cuts, fiscal concerns, and a potential return of Trump’s “Weak USD Doctrine” by H2 2025.

CHF: Safe-haven flows have bolstered the CHF amid Eurozone uncertainties. Once risks subside, the CHF could return as a funding currency, supported by near-zero rates and high valuations. The SNB will monitor FX developments amid Swiss disinflation.

JPY: The JPY remains resilient, with the US-Japan rate spread narrowing as the Fed cuts rates and the BoJ hikes. This reduces USD/JPY carry appeal, with volatility likely to persist due to rate path uncertainties and Trump’s trade policies. Japan’s MoF may intervene to support the JPY.

GBP: UK economic concerns and high borrowing costs could necessitate austerity, creating headwinds. However, political stability and economic outperformance relative to the Eurozone support GBP as a higher-yielding EUR proxy. GBP/EUR is constructive for 2025-2026, while GBP/USD may recover in 2026 after initial struggles.

CAD: USD/CAD hit highs above 1.45 due to Trump’s tariffs, but risks remain tilted downward for CAD in early 2025 amid a wider BoC-Fed rate gap. Canada’s relative growth outperformance could aid a gradual CAD recovery.

AUD/USD: Trump’s China tariffs and a falling rate differential weakened AUD/USD, but softer tariffs and less dovish RBA policy could provide support.

NZD/USD: NZD/USD was pressured by China tariffs, a falling NZ-US rate differential, and dry weather. Lower-than-expected tariffs, stable rate differentials, La Niña, and NZ growth rebound should support NZD/USD.Publication date:

2025-02-28 12:25:54 (GMT)

The terms and conditions of use set out below (referred to as "FX Blue's Terms"), form a contractual agreement governing FX Blue's relationship with you in relation to your use of this Website (“Agreement”) and you agree to be legally bound by FX Blue's Terms just as if you had signed this Agreement. By using this Website and any Information, you are agreeing to comply with and be bound by FX Blue's Terms, including any revisions that may be made to FX Blue's Terms from time to time. FX Blue reserves the right, in FX Blue's sole discretion, to change, modify, add or remove portions of FX Blue's Terms at any time by posting the revisions on the Website. You should check FX Blue's Terms periodically for changes as by using the Website after FX Blue posts any changes to FX Blue's Terms, you are agreeing to accept those changes, whether or not you have reviewed them, and you waive any right you may have to receive individualised notice of such changes. FX Blue's Terms may be supplemented by additional terms and conditions pertaining to specific content and activities. You agree and understand that such additional terms and conditions are hereby incorporated by reference to FX Blue's Terms. Your continued use of the Website means that you accept any new or modified FX Blue Terms.